The Stablecoin Paradox

Stablecoins could win up "kneecapping" your favorite blockchain

Executive Brief

Overview: Stablecoins are crypto's most successful product, enabling over $30 trillion in on-chain value transfer annually. Yet their growth reveals a deeper paradox: the most scalable use case in decentralized finance is a highly centralized, dollar-denominated asset that operates under increasing regulatory scrutiny. This brief distills key insights from our full-length report on the stablecoin market.

Key Insights:

USD Stablecoins Dominate the Market

Over 99.8% of all stablecoins are pegged to the U.S. dollar.

Crypto's killer app is a fiat derivative.

Emerging markets drive demand due to currency instability and limited banking infrastructure.

Stablecoins Are Powering Global Payment Infrastructure

Stablecoins are disrupting cross-border B2B payments, treasury ops, and remittances.

Real settlement time: seconds. Cost: pennies.

Still limited by shallow liquidity, off-ramp friction, and emerging regulatory conditions.

While Currently Murky, Regulatory Clarity is Arriving

The GENIUS Act and STABLE Act propose dual state/federal frameworks with strict 1:1 reserve and audit requirements.

Compliant stablecoins will not be regulated as securities or commodities.

Decentralized and algorithmic stablecoins may struggle to survive.

Centralization is Winning Over Decentralization

Most stablecoins are issued and controlled by centralized entities.

They comply with law enforcement and increasingly integrate into traditional financial systems.

Decentralization has become a secondary concern for users seeking speed, access, and stability. This centralization will most likely bleed into most assets and chains.

Abstract

Stablecoins are rapidly becoming one of the most significant innovations in global finance, quietly powering trillions in value transfer across decentralized networks while straddling the divide between traditional finance and crypto-native infrastructure. Stablecoin news, growth, adoption, launches, etc., have exploded in the last year. Fidelity, Wyoming, and Trump: all launching stablecoins. Stablecoin market cap reaches all-time highs. Circle looks to IPO. Imminent stablecoin regulation is on the horizon.

But they are not without controversy. Their rise reveals deep tensions between decentralization and control, innovation and regulation, permissionless systems, and real-world compliance. Despite their roots in a movement built on autonomy and censorship resistance, stablecoins are increasingly defined by central issuers, regulatory clarity, and national interest. This report examines those contradictions head-on, asking not only how stablecoins work but what they ultimately mean for the future of crypto, markets, and monetary sovereignty.

A Quick Recap on Stablecoins

Stablecoins are simple in name and complex in design. At their core, they are blockchain-based tokens engineered to mirror the price of a fiat currency, typically the US dollar. But behind the scenes, maintaining that 1:1 peg requires a delicate balance of trust, mechanisms, and collateral. Understanding how these components fit together is essential for anyone analyzing the stablecoin market.

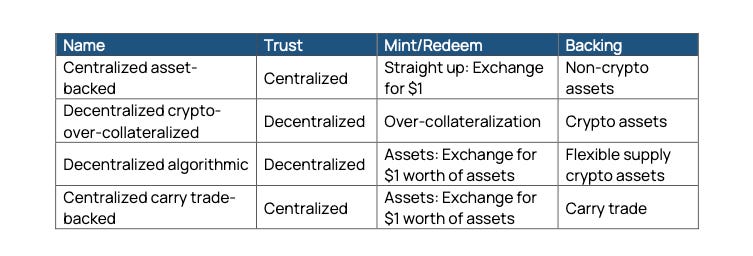

Three Pillars of Stability

1. Trust: Centralized vs. Decentralized

The trust model defines who controls the stablecoin’s issuance and collateral. Stablecoins can either be:

Centralized: Managed by an issuing company that holds custody of the underlying assets and enforces the peg through internal controls. These systems rely on user trust in the issuer's solvency, transparency, and regulatory compliance.

Decentralized: Governed by smart contracts and DAOs, where rules are enforced by code. Here, transparency is built into the system, but so is risk, particularly around collateral volatility and governance attacks.

2. Mint and Redeem Mechanisms

How stablecoins are created and destroyed is just as important as what backs them. There are three primary mint/redeem structures:

A. Straight Dollar Exchange

The most direct method: one stablecoin is always minted or redeemed for one dollar. This 1:1 mechanism relies on arbitrage to keep the price anchored. When the market price drifts above or below the peg, arbitrageurs step in to restore parity, profiting from the spread and maintaining equilibrium.

B. Asset-for-Dollar Exchange

Instead of fiat, users provide one dollar’s worth of a pre-approved asset, such as USDC, ETH, or other tokens, to mint one stablecoin unit. While this approach mimics the straightforwardness of the dollar exchange, the stability of the peg now depends on the resilience of the asset being used. If confidence in the asset drops, the system becomes vulnerable to redemptions and potential death spirals.

C. Over-Collateralization

Used by decentralized projects like DAI, this method requires users to lock up more than one dollar’s worth of collateral to mint a single stablecoin. The protocol enforces a minimum collateral ratio, often above 150 percent, to absorb volatility and preserve solvency.

If the collateral value drops and breaches a critical threshold, liquidation auctions are triggered. These auctions sell the collateral to burn outstanding stablecoins and restore the system’s over-collateralized status. The stability here comes from excess reserves and incentive alignment, not from simple parity.

However, this structure often needs supplementary stabilization mechanisms, like savings rates or peg buffers, to remain effective over time.

3. Backing: What Anchors the Value

The nature of the reserve assets determines the true robustness of the stablecoin. These can be grouped into four broad categories:

A. Non-Crypto Assets

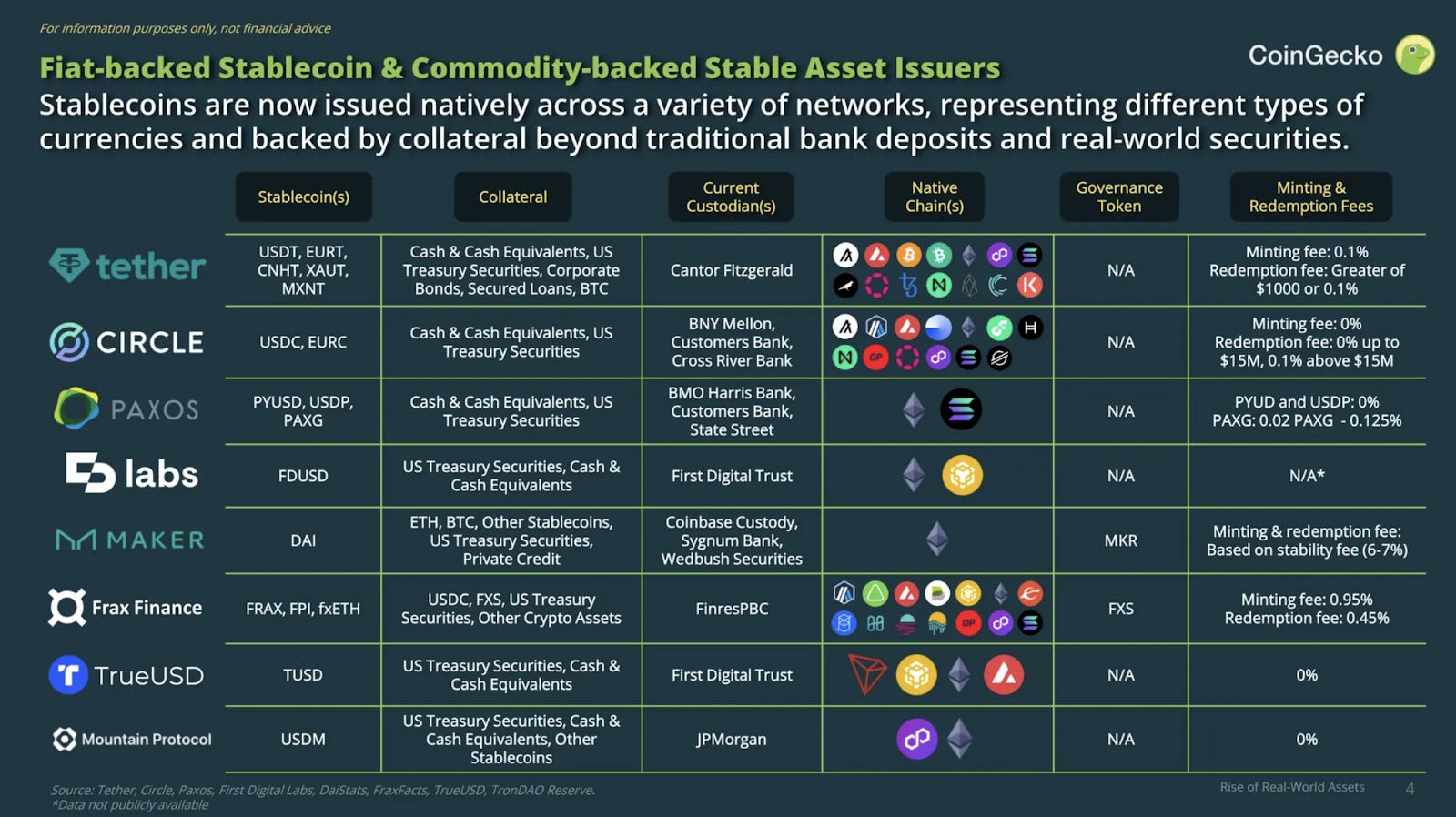

These include traditional financial instruments such as cash, treasury bills, commercial paper, and bank reserves. This category underpins most centralized stablecoins like USDT and USDC, offering regulatory familiarity and low volatility, but also regulatory exposure and opacity risks.

B. Crypto Collateral

These are digital assets used in decentralized protocols, such as ETH or wrapped tokens. The challenge here lies in their inherent volatility, which often requires over-collateralization and constant rebalancing.

C. Flexible Supply Tokens

Some experimental stablecoins use reflexive mechanisms where the backing asset expands or contracts in supply to maintain the peg. These systems attempt to algorithmically manage demand and supply, often without direct collateral. While elegant in theory, they remain fragile in periods of market stress.

D. Carry Trade Strategies

This backing model relies on profiting from the price difference between spot and futures markets. By simultaneously holding the underlying asset and shorting its future, the issuer captures the spread as yield. Though potentially lucrative, this introduces market timing and execution risk and resembles hedge fund behavior more than traditional collateralization. Ethena (USDe) is the most famous example.

Takeaway

Stablecoins may all aim for a one-dollar value, but their methods for achieving that target differ radically. Whether they lean on trust in an institution, clever contract design, or capital efficiency, each category comes with trade-offs in stability, transparency, scalability, and systemic risk.

Understanding these foundational mechanics is not just helpful, it is essential. The nuances behind trust, minting logic, and backing assets determine which stablecoins thrive in calm markets and which ones survive in chaos.

Why Are Stablecoins Making Headlines Now?

Stablecoins, once relegated to the realm of niche crypto products, have rapidly evolved into a key pillar of the modern financial ecosystem. Their journey from a tool for crypto traders to a transformative global financial instrument has been swift and unprecedented. The surge in attention surrounding stablecoins is not simply a byproduct of market speculation or fleeting trends. They’ve found product-market fit, demonstrated explosive growth, and benefited from increasing regulatory clarity—factors that collectively position them at the intersection of policy, fintech, and institutional strategy.

Unprecedented Growth: Volume, Velocity, and Validation

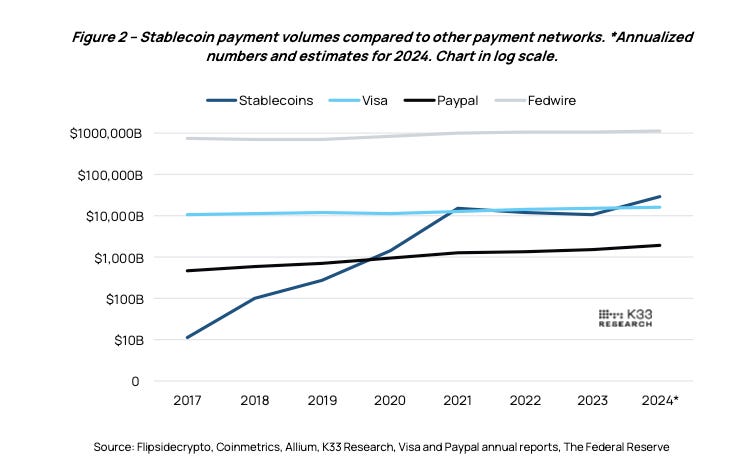

The most tangible measure of stablecoin adoption is the sheer volume of on-chain activity. In 2023, stablecoins facilitated over $10 trillion in transactions across 2.5 billion transfers, a figure that skyrocketed to $30 trillion in 2024, with nearly 4 billion transactions. These numbers transcend theoretical use cases; they represent real value moving across decentralized networks at scale. While stablecoins’ transaction volumes have matched or exceeded the levels seen by traditional payment systems like Visa, 2024 may well mark an inflection point in their trajectory. Stablecoins surpassed PayPal’s payment volume in 2020 and eclipsed Visa’s by 2021. However, in comparison to interbank settlement systems like Fedwire—which processed an astonishing $1,100 trillion in 2023—stablecoins still operate on a smaller scale.

Nevertheless, drawing direct comparisons between stablecoin networks and traditional payment systems is fraught with complexity. The stablecoin ecosystem handles fewer transactions than Visa or PayPal, but the average transaction size is far greater. In 2023, Visa processed 276 billion payments, averaging $54 each, while PayPal saw 25 billion transactions, averaging $61. In contrast, Fedwire managed just 193 million transactions, each averaging $5.6 million. Stablecoins, with 2.6 billion transactions in 2023, had an average transfer size of $4,200, spanning a middle ground between retail and institutional usage.

Three dominant categories emerge from this activity:

Trading-related transactions, including arbitrage and liquidity provisioning

Internal transfers, often between wallets or within smart contracts

Payments and remittances, particularly in cross-border value transfer

Notably, around 95% of stablecoin transaction volume consists of transfers above $10,000, underscoring the dominance of institutional trading and internal consolidation. But beneath the surface, a more retail-like ecosystem is quietly gaining traction, with 70% of all transactions valued under $1,000.

Regulatory Winds Shift in Favor of Stablecoins

Stablecoins are becoming increasingly important, with regulators around the world developing frameworks to integrate them into financial law. By 2025, a clearer regulatory environment is emerging, particularly for USD-pegged stablecoins. While some ambiguity remains, the U.S. Securities and Exchange Commission (SEC) has provided clarity by stating that certain fiat-backed stablecoins, such as those fully backed by U.S. dollars and used primarily for payments, are not considered securities. This distinction—referred to as “Covered Stablecoins”—exempts such assets from investment regulations, provided they meet certain criteria, including proper reserves and non-profit marketing. This decision is a key milestone, unlocking the doors to broader institutional engagement. However, Tether (USDT) likely falls outside this classification due to its reserve structure.

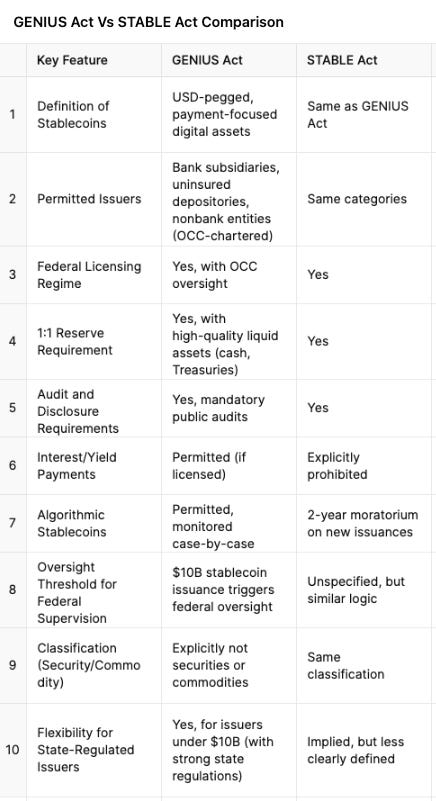

Additionally, Congress has introduced the GENIUS Act, which creates a legal framework for fiat-backed stablecoin issuers and explicitly exempts them from SEC and CFTC jurisdiction. This bill also establishes a licensing regime for issuers and mandates full 1:1 reserves and regular audits. In contrast, the STABLE Act, introduced in the House, bans stablecoins from paying interest or yield and imposes a two-year moratorium on algorithmic stablecoins.

The legislation brings much-needed clarity, protecting consumers and ensuring stablecoin stability, while encouraging innovation, such as the potential for nonbanks to issue stablecoins. Globally, regions like Japan and Hong Kong are implementing robust regulatory frameworks, while Latin America sees widespread, grassroots stablecoin adoption amidst regulatory uncertainty.

In summary, stablecoins are moving toward a more regulated future, with the U.S. and other regions providing clarity and creating opportunities for innovation, though challenges remain in terms of international consistency and user adoption in developing markets.

Tokenization Is the Trojan Horse, and Stablecoins Lead the Charge

The push for tokenization is rapidly becoming one of the most significant shifts in global finance. When BlackRock—one of the largest asset managers globally—declares that “everything will be tokenized,” it signals that this movement is no longer the exclusive domain of crypto enthusiasts. The launch of BlackRock’s BUIDL fund, a tokenized basket of U.S. Treasuries, exemplifies how this vision is materializing.

However, despite this institutional enthusiasm, public perception of crypto remains tainted by the sector's tumultuous past. The collapses of FTX, yield farms, and the widespread loss of user funds during 2021-2022 have left lasting scars. Even with developments like the approval of Bitcoin and Ethereum spot ETFs, public trust in crypto remains fragile.

Stablecoins are positioned to bridge this gap. Their inherent structure is simple, and their use case is readily understandable. They function like traditional fiat currencies but are programmable, transferable, and open, offering a clean, digestible entry point into the tokenized financial ecosystem. This has not only caught the attention of fintech companies but also regulators and institutions, which are increasingly eager to incorporate stablecoins into their offerings.

Fintech’s Next Frontier

Rather than disrupting traditional fintech, stablecoins are seamlessly integrating into the existing infrastructure. PayPal has already launched its own stablecoin, PYUSD, which is now integrated across multiple blockchains and DeFi protocols. Visa has piloted programs to settle card payments using USDC, and Stripe is now entering the fray.

Rather than emerging as a disruptive force, stablecoins will likely be incorporated into existing financial systems through established players:

Payment facilitators like Stripe and Block are enabling stablecoin-based checkout options, improving merchant margins

Super apps like Venmo, Cash App, and Klarna are extending their functionality to include stablecoin wallets and payouts

Device manufacturers like Apple and Google, with their built-in wallet infrastructure, are well-positioned to drive mass adoption

Shopping platforms and next-gen banks are developing hybrid accounts that merge fiat and crypto seamlessly

In 2024, Stripe made headlines by acquiring Bridge, a stablecoin infrastructure company, for $1.1 billion, marking its largest acquisition to date. Stripe’s return to crypto, after previously abandoning Bitcoin in 2018, is telling. This time, the focus is not on speculative assets but on the infrastructure layer that could one day replace traditional payment systems.

The Case for Stablecoins: Why They Matter

As digital representations of fiat currency designed to move across decentralized rails, stablecoins offer a rare combination of trust, utility, and scalability. Whether acting as transactional middleware, programmable financial infrastructure, or a tool for global dollarization, stablecoins are emerging as one of the most consequential inventions in modern finance.

Their benefits fall across several distinct but overlapping domains: stability, accessibility, transparency, efficiency, and geopolitics.

Stability in Volatile Environments

Stablecoins provide a rare ability to hold value in markets prone to inflation and currency volatility. In countries like Venezuela, Nigeria, or Turkey, stablecoins serve as digital lifelines, offering individuals access to U.S. dollar-denominated savings while circumventing capital controls, corrupt banking systems, and inflationary pressures. For those without access to traditional banking systems, stablecoins offer a permissionless and open route to dollar exposure.

But this benefit isn’t confined to geographic instability. Within crypto’s inherently chaotic environment, stablecoins offer much-needed predictability. For DeFi users, market makers, and arbitrageurs, stablecoins are safe harbor amid speculative storms. They allow users to operate within crypto-native environments without assuming crypto-native risk.

Accessibility, Interoperability, and Financial Inclusion

Stablecoins bypass the limitations of legacy financial systems. They move seamlessly across public blockchains without being confined to jurisdictional boundaries or banking hours. Unlike traditional payment apps, stablecoins are interoperable by default and able to move between wallets, platforms, and protocols without friction.

This makes them particularly appealing in markets where financial infrastructure is fragmented or exclusionary. Instead of relying on siloed fintech apps or costly correspondent banking systems, stablecoins provide a unified, 24/7 alternative.

Transparency, Real-Time Audibility, and Programmability

The on-chain transparency of stablecoins offers significant advantages over traditional financial systems, where transactions and reserves are often opaque. This level of visibility has made stablecoins attractive not only to institutions but also to regulators and compliance teams. While they don’t eliminate risk entirely, the traceability of stablecoin transactions provides an unprecedented level of clarity.

Perhaps the most underappreciated benefit of stablecoins is their programmability. As smart contract-enabled money, they can embed logic at the payment layer, automating compliance, real-time tax withholding, or enforcing payment conditions. This opens the door to a future of composable, customizable, and always-on financial services.

Superior Settlement for Cross-Border Transactions

The clearest competitive edge stablecoins have today is in cross-border payments. Traditional models, correspondent banking, money transmitters, and payment aggregators are riddled with high costs, regulatory overhead, and intermediaries.

Stablecoins collapse this complexity. They allow two parties in different countries to settle transactions in near real-time, without relying on expensive financial institutions or multi-step clearing networks. While they do not yet replace first-mile or last-mile distribution systems, they significantly reduce the middle-mile friction that characterizes most cross-border value transfers.

For this reason, stablecoins are poised to become the preferred settlement layer for global commerce, particularly for emerging fintech platforms and remittance corridors.

Monetary Policy, Reserve Currency Power, and the Dollar’s Reach

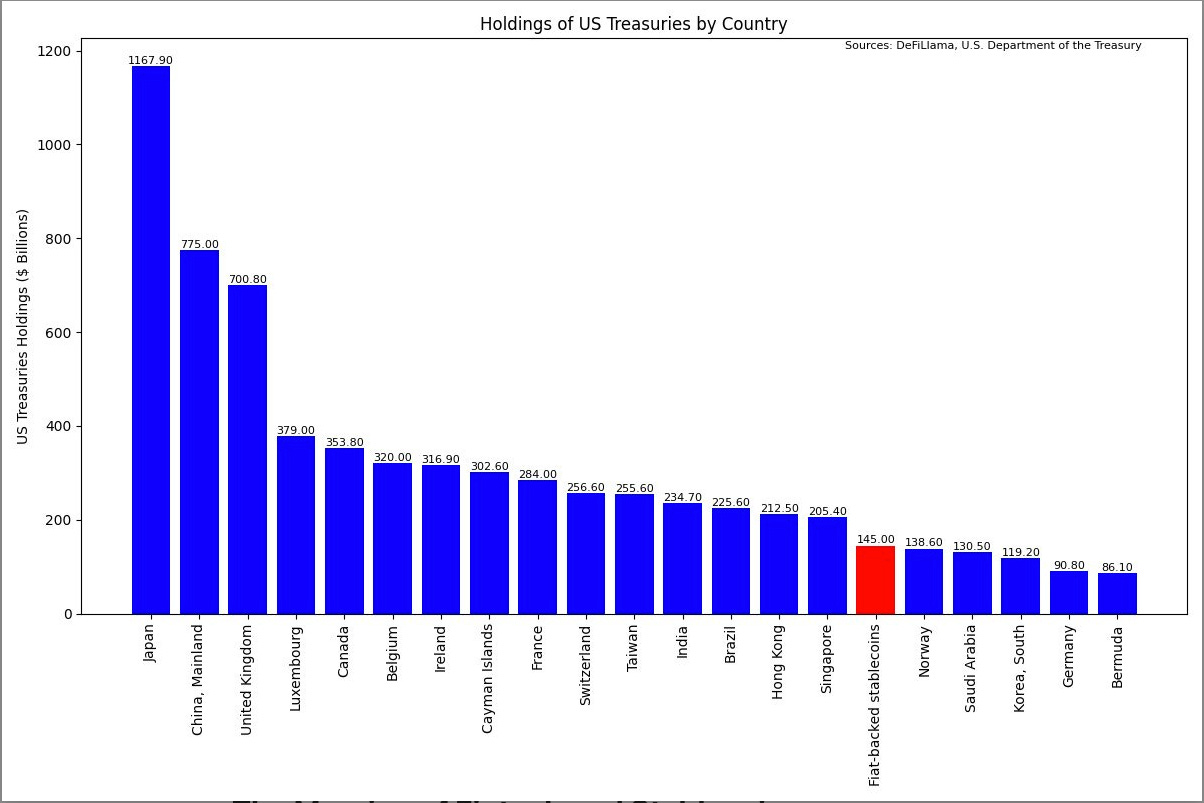

A crucial, often overlooked aspect of stablecoins is their geopolitical impact. With over 99% of stablecoins denominated in U.S. dollars, stablecoins are accelerating the dollarization of the global financial system, extending U.S. dollar liquidity into digital ecosystems and emerging markets. This trend reinforces the dollar’s dominance as the global reserve currency, providing increased demand for U.S. treasuries, with stablecoins holding more than any country except a handful of sovereign states.

However, this success comes with a potential downside. If stablecoins begin disintermediating banks and pulling deposits from the institutions that underpin the fractional reserve system, their success could undermine the very foundations of the financial system they support.

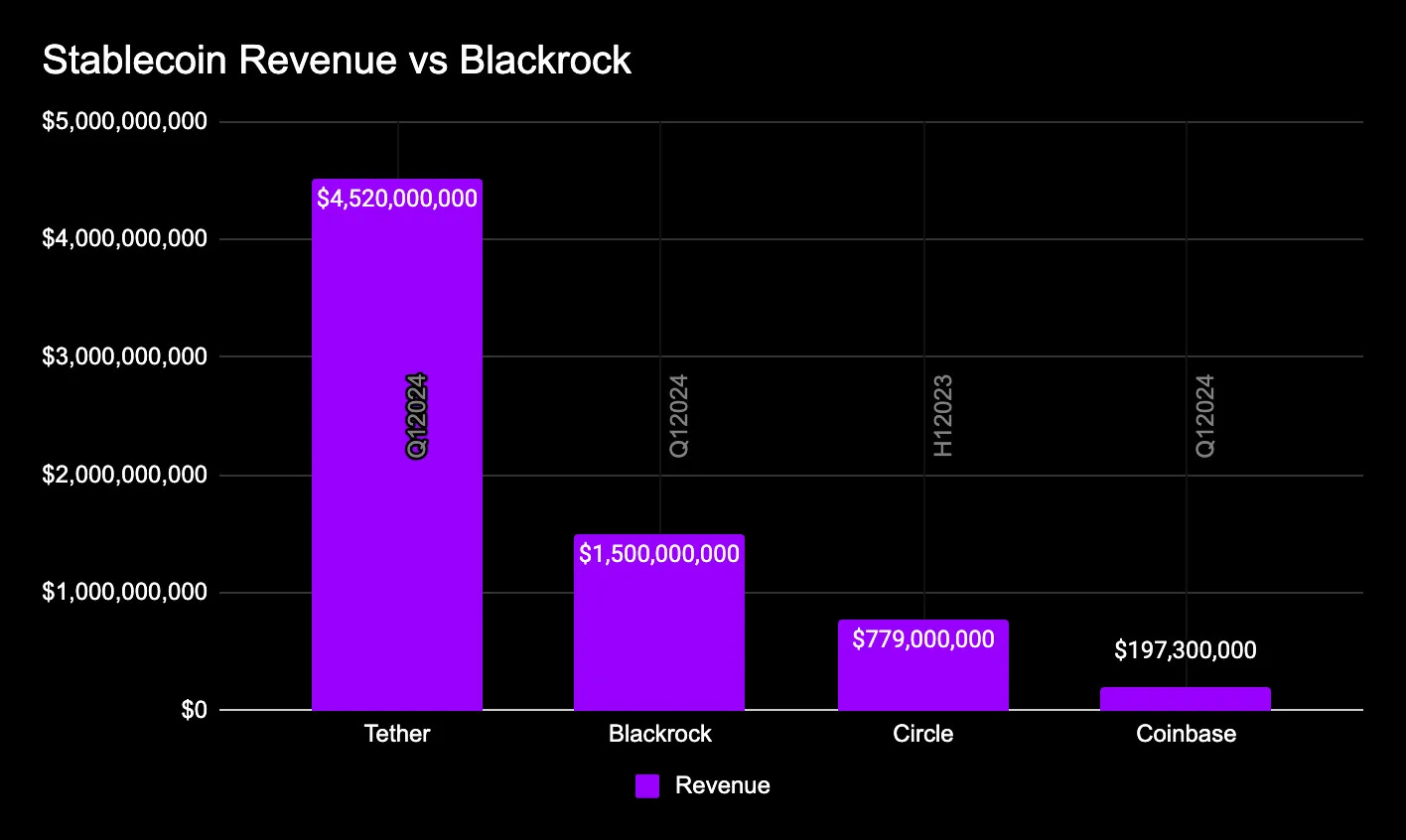

Revenue for Issuers and Infrastructure Builders

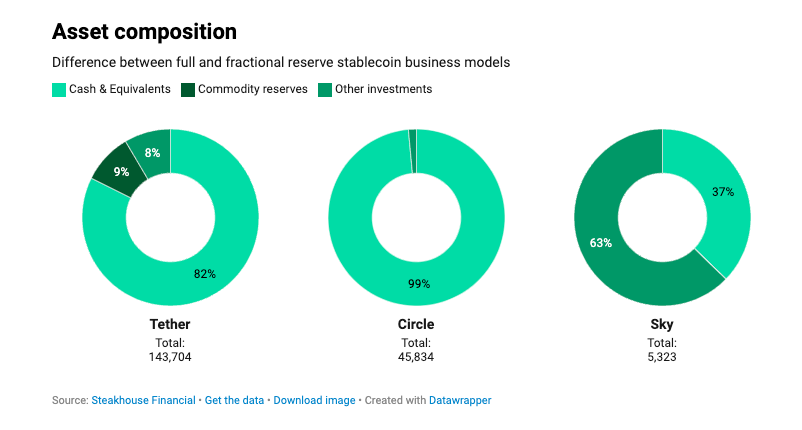

Stablecoin issuers are not public utilities. They are businesses that can be highly profitable. Tether reported over $5 billion in net profit in the first half of 2024, while Circle is preparing for a multibillion-dollar IPO. Most of this revenue comes from holding yield-generating assets like T-bills while paying depositors zero.

The rise of these products reveals an important insight: value accrues to the issuer, not the stablecoin itself. Investors in the stablecoin ecosystem are increasingly focused on infrastructure and platforms, not just price-pegged tokens.

However, the jaw-dropping revenues/valuations may not last forever as competition heats up and interest rates (potentially) fall. Circle’s IPO filing has peeled back the curtain on the harsh financials behind even the most prominent issuers. Soaring operational costs (over $250 million in annual compensation and another $140 million in general expenses) combined with narrowing gross margins and overreliance on yield from interest-bearing assets paint a challenging picture. Its proposed $5 billion valuation (roughly 32x projected 2024 earnings) is steep by most measures.

As margins compress and competition intensifies, issuers are shifting toward vertical integration and specialized infrastructure. Codex exemplifies this next phase: a blockchain purpose-built for stablecoin transactions, betting that general-purpose chains can't match the throughput or cost-efficiency required for scaled operations. Whether this specialization offers a sustainable edge remains to be seen.

Use Cases of Stablecoins

Stablecoins have rapidly transitioned from niche tools to foundational elements within both the crypto ecosystem and the broader global financial landscape. Initially developed to overcome barriers imposed by traditional banking systems, stablecoins are now driving critical financial infrastructure. Their role extends across crypto trading, cross-border B2B payments, remittances, treasury management, and even domestic retail transactions. This diversification highlights not only the utility but also the substantial economic value stablecoins are bringing to various sectors.

Trading: The Genesis and Dominant Use Case

Stablecoins’ emergence was catalyzed by a key pain point in the early crypto ecosystem: access to fiat banking. In its nascent stages, converting fiat into crypto was a convoluted and expensive process. Many exchanges operated with "crypto-only" models, unable to establish banking partnerships for fiat deposits via traditional methods like ACH or wire. As a result, users turned to peer-to-peer services or third-party platforms to bridge this gap.

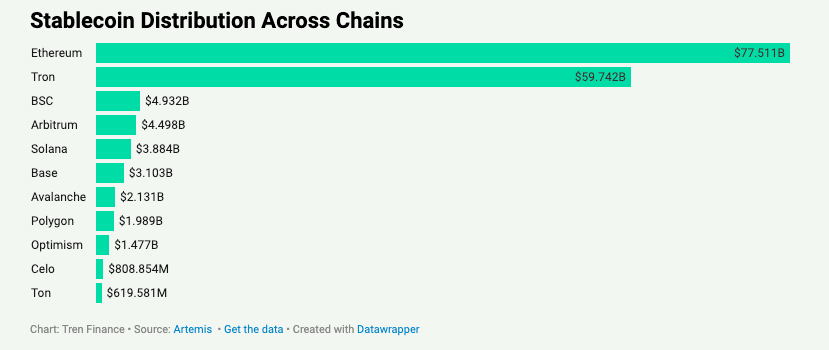

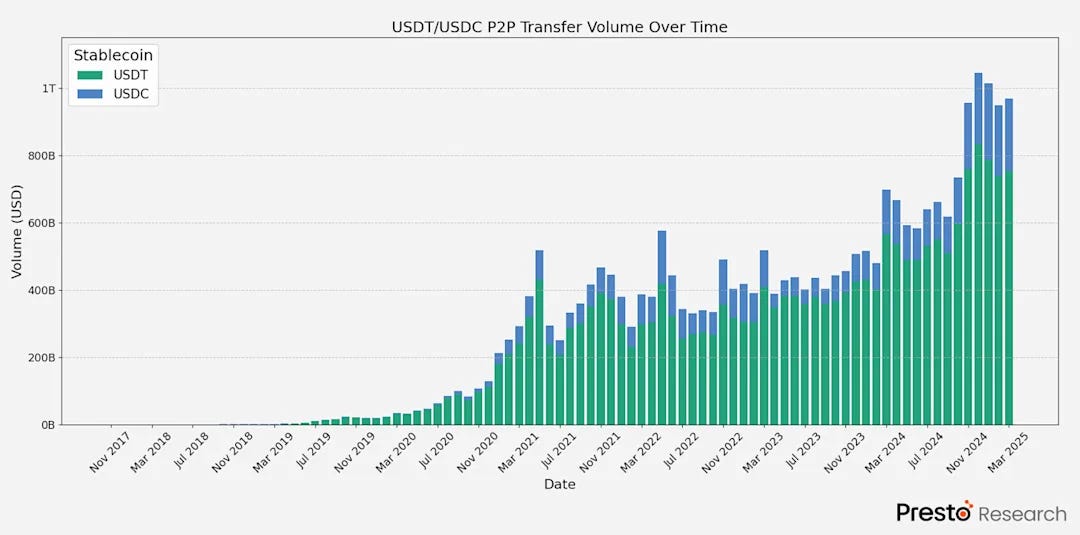

Enter Tether (USDT), which effectively became the de facto solution. It allowed crypto exchanges to offer dollar-denominated trading pairs without requiring direct banking access. USDT's adoption skyrocketed (primarily on Ethereum and Tron, the image below), especially in regions like Asia, where access to fiat gateways was even more limited. Meanwhile, Western exchanges like Coinbase and Kraken secured banking relationships and launched native USD pairs to differentiate themselves.

Today, Tether remains the most traded asset globally, consistently surpassing Bitcoin and Ethereum in transaction volume, a testament to its entrenched role in crypto trading. Exchanges like Binance, OKX, and Bybit still rely heavily on USDT, while platforms like Coinbase, Gemini, and Kraken lead fiat-accessible markets.

Stablecoins as a Disruptive Rails Layer

Stablecoins provide a radical alternative to the traditional payment infrastructure. By leveraging crypto wallets and neutral blockchains, stablecoins enable near-instant cross-border transactions for a fraction of the cost. They eliminate intermediaries, market hours, and pre-funded accounts, transforming the payment landscape.

Four core features make stablecoins an ideal solution for global payments:

Disintermediation: Blockchain technology allows direct transactions between senders and receivers without the need for multiple institutions to approve, settle, or reconcile payments. This dramatically reduces fees and shortens settlement times from days to seconds.

Programmability: Cross-border payments are more than just fund transfers; they are part of business workflows that include approvals, compliance checks, and risk management. Stablecoins enable these processes to be automated and encoded within smart contracts. This approach allows decentralized exchanges like Uniswap to settle billions in trades with minimal human intervention.

Fraud Prevention and Compliance: Blockchain’s transparency and cryptographic identity layers reduce fraud risk. Chargebacks, which plague B2C payments, are less of a concern in B2B transactions, and stablecoins’ atomic, irreversible settlement improves security compared to traditional systems.

Capital Efficiency: Stablecoins eliminate the need for capital to be locked in multiple jurisdictions. According to BVNK, $11.6 billion is tied up in just four major B2B payment corridors, and around $5 trillion sits idle in pre-funded accounts. Stablecoins release this capital, allowing businesses to unlock productivity and reduce costs.

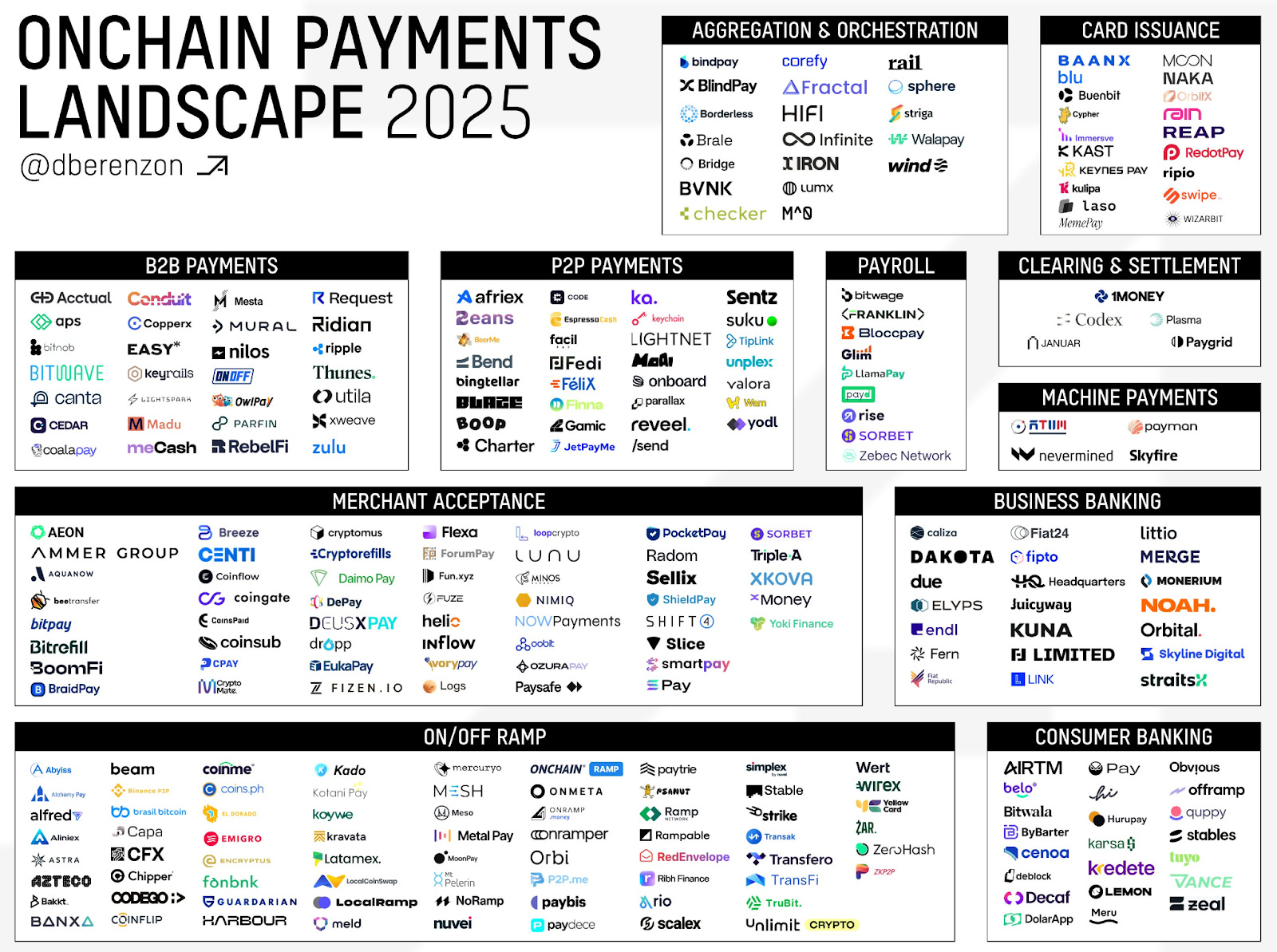

The Stablecoin Payments Stack: Who Benefits?

As the stablecoin ecosystem matures, the value will shift across the payments stack:

Wallet providers will monetize through yield sharing, premium services, and data

Merchants will save on fees and capture investment income

Infrastructure providers, including on/off ramps, compliance platforms, and stablecoin issuers, will control the operational layer

Blockchains will accrue transaction volume and establish themselves as settlement layers

Cross-Border B2B Payments: A $150 Trillion Market in Transition

Stablecoins are poised to disrupt one of the largest and most inefficient sectors of global finance: cross-border B2B payments. In 2023, cross-border payments totaled between $156 trillion and $190 trillion, with B2B transactions accounting for $39 trillion to $150 trillion of that total. This segment is expanding rapidly due to the growth of global eCommerce and digital services. However, the existing infrastructure is woefully outdated.

The SWIFT network, which has been the backbone of international payments since 1973, is burdened by long settlement times (2-5 business days) and high fees (typically 4-6%). Additional costs are buried in FX spreads, compliance overhead, liquidity fragmentation, and reconciliation issues. Meanwhile, the infrastructure that underpins SWIFT’s operation is increasingly out of sync with the demands of a modern, globalized economy.

Stablecoins Transform Person-to-Person Transfers

Stablecoins are also revolutionizing the person-to-person (P2P) transfer market. While developed nations benefit from relatively efficient payment systems, these systems are still prone to inefficiencies. Credit card networks, issuing banks, and payment processors all take a cut, and transactions can still take days to settle. Meanwhile, closed-loop systems like PayPal, WeChat Pay, and Starbucks offer convenience but suffer from interoperability challenges and fragmented ecosystems.

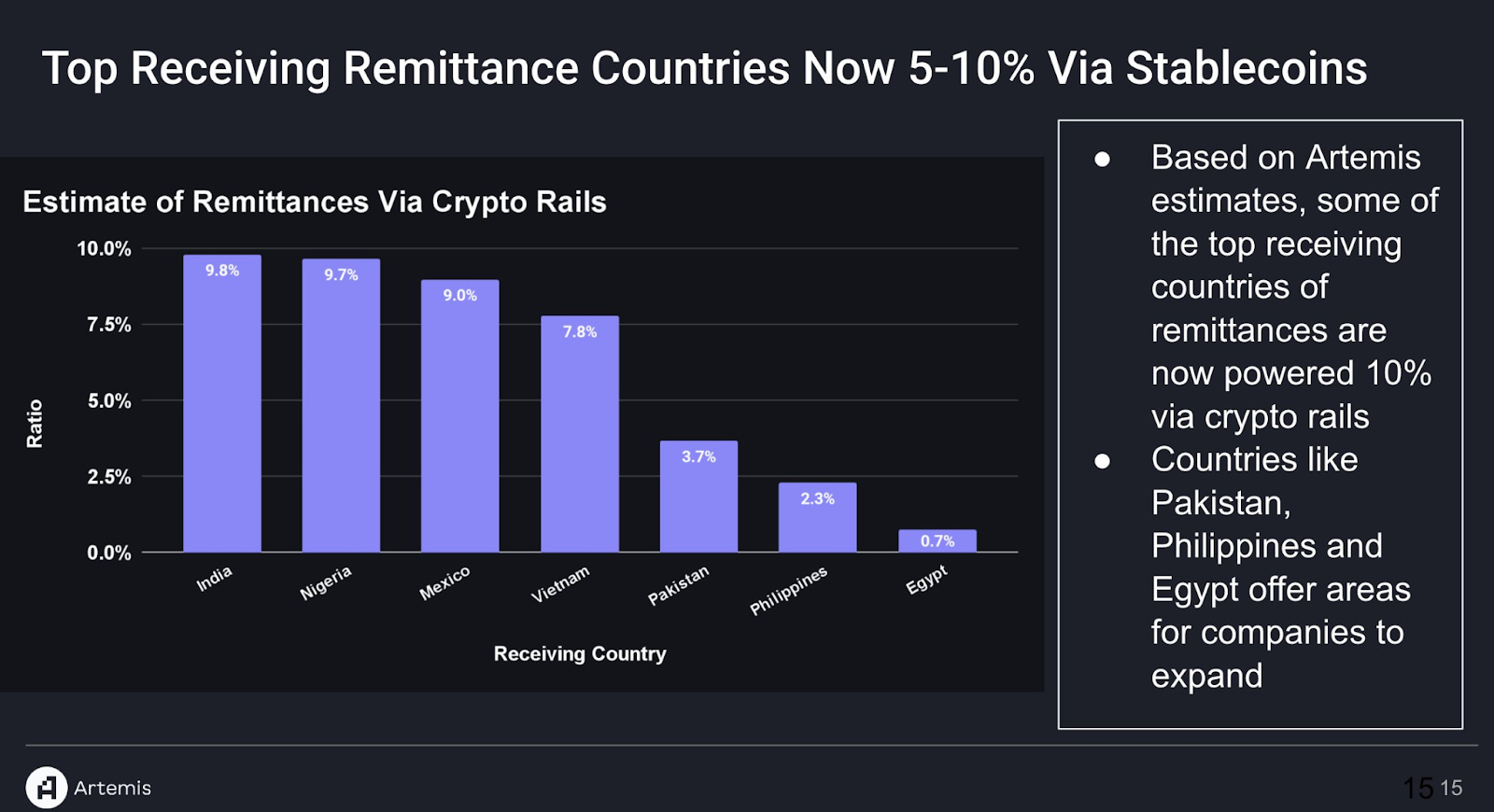

Stablecoins solve these problems. In regions where remittance costs exceed 7% and transfers take several days, stablecoins offer a cost-efficient and instantaneous alternative, settling transactions in minutes for under 1% in fees.

Emerging markets are the most significant beneficiaries. Stablecoins provide access to dollar-based income streams for freelancers, contractors, and gig workers in unstable economies. They also shield savings from hyperinflation and currency devaluation, bypassing capital controls and providing a route to dollarization.

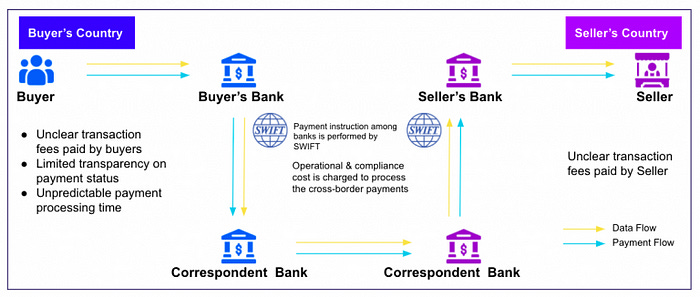

Why SWIFT and Correspondent Banking Are the Bottlenecks

SWIFT is not a payment system. It is a messaging network used by financial institutions to coordinate payments. The actual money movement happens via correspondent banks, which maintain bilateral accounts (nostro/vostro) across jurisdictions. These banks facilitate local payouts and FX conversions, each introducing their own fees, compliance processes, liquidity requirements, and operational delays.

The costs add up quickly:

SWIFT messaging fees

Multiple layers of intermediary bank charges

FX conversion spreads (1–2%)

Reconciliation delays

Capital inefficiency from pre-funded accounts

Fraud and compliance overhead

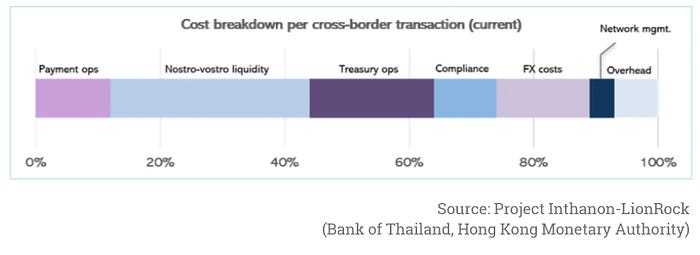

A Bank of America report on Wise estimated that 75% of the cost in cross-border transactions comes from treasury ops, fraud prevention, and compliance. Add to that billions in working capital trapped for days, capital that could otherwise be earning yield or deployed into operations.

Even high-quality corridors like the US–UK are inefficient. For more exotic corridors (e.g., Brazil to Southeast Asia), the experience deteriorates rapidly.

Treasury, Payroll, and Global Business Operations

Enterprises are beginning to use stablecoins not just for payment, but for treasury. Firms like Starlink are replacing fragmented pools of working capital with stablecoin balances that can be distributed globally and converted instantly.

Instead of managing 30+ bank relationships, a business can hold one stablecoin balance and settle to counterparties worldwide in real-time. This improves working capital, eliminates FX risk, and simplifies accounting.

Digital service providers, SaaS companies, and global content platforms are following suit. Stablecoins allow them to serve customers and pay contractors in new markets without building traditional banking infrastructure.

Drawbacks of Stablecoins

Stablecoins have undeniably become one of the most transformative innovations in modern finance, offering a new way to transfer, store, and utilize value in the digital world. From their humble beginnings as a solution to banking barriers in the early days of crypto, stablecoins have expanded into a critical infrastructure layer for cross-border payments, decentralized finance (DeFi), and digital commerce. Despite their promise and widespread adoption, however, they remain far from flawless. The deployment of stablecoins in real-world applications continues to face significant operational, structural, and ideological challenges. These obstacles aren’t just temporary setbacks; they reflect deeper tensions within the crypto ecosystem's broader ambition to create a parallel financial system. This piece explores the limitations of stablecoins, their unintended consequences, and their potential impact on both the crypto ecosystem and the traditional financial world.

Cross-Border Limitations: Liquidity, Off-Ramps, and Regulatory Bottlenecks

While stablecoin transactions can settle instantly on the blockchain, the reality of global cross-border payments often relies on centralized exchanges (CEXs) and thinly traded corridors. In markets with low liquidity, large transactions can deplete available order books, leading to poor execution prices or requiring transactions to be rerouted through over-the-counter (OTC) markets. This not only adds complexity and cost but also delays the settlement process. In less developed crypto markets, this issue is even more pronounced, with market makers hesitant to engage in stablecoin foreign exchange (FX) pairs due to the high opportunity costs. Volatility trading and DeFi arbitrage offer higher returns, leaving stablecoin transactions underserved.

Offboarding Frictions

Even when a stablecoin transaction is successfully completed on-chain, converting that stablecoin into fiat currency can be a major bottleneck. Many countries still lack modern payment systems or real-time settlement infrastructure, meaning that the final “last mile” of the transaction can take days. For example, a cross-border transfer made on the weekend might not be accessible in fiat until the following business day due to banking hours. In regions without deep liquidity or institutional market participation, these delays cannot be efficiently arbitraged, meaning that cross-border payments remain slower and more expensive than they could be.

Regulatory Uncertainty: The U.S. and Global Capital Controls

A significant underlying issue is the regulatory environment, particularly in the United States. The absence of clear guidelines or safe harbor provisions leaves traditional financial institutions—such as banks, payment processors, and foreign exchange (FX) dealers—reluctant to enter the stablecoin ecosystem. These institutions could provide the depth and scale necessary to make stablecoins a true global liquidity solution, but regulatory ambiguity remains a substantial barrier to entry. Until these institutions are properly authorized and incentivized to handle stablecoin transactions, liquidity and off-ramp issues will persist.

Adding to this challenge, stablecoins are predominantly denominated in U.S. dollars, making them an attractive tool for dollarization but also a target for governments enforcing capital controls. In regions with restrictive capital policies, stablecoins are likely to face regulatory opposition, especially in consumer remittances, where dollarization can undermine local currency sovereignty. However, for B2B transactions, the regulatory environment is more conducive to stablecoin adoption as alignment with international standards becomes increasingly feasible.

Unintended Consequences Across Global Stakeholders

The rise of stablecoins has profound implications for various global stakeholders, with both positive and negative effects. For banks and financial institutions, stablecoins represent a threat of disintermediation, particularly as users bypass traditional deposit-taking banks in favor of interest-bearing stablecoin products. As this shift accelerates, margin compression and decreased deposits are likely outcomes for these legacy institutions.

For fintechs, stablecoins provide new revenue streams, but they also introduce competition from decentralized solutions that bypass traditional banking systems. Regulatory agencies face the complex task of balancing traceability and enforcement while also dealing with the complexities of global financial flows enabled by stablecoins. Governments, particularly in countries with weak currencies, may see stablecoins as a threat to their monetary sovereignty as users increasingly opt for dollar-denominated stablecoins over local currencies.

For global businesses and consumers, stablecoins offer greater financial access, particularly in regions with an underdeveloped banking infrastructure. Yet, the lack of clear regulatory frameworks in many countries creates uncertainty and risks for users, particularly in politically sensitive regions where stablecoins could exacerbate inflation or undermine national currency control.

The Centralization Problem: Control, Fragmentation, and Ideological Drift

While stablecoins have introduced the concept of programmable dollars to the crypto ecosystem, they also present a significant centralization problem. Many of the most prominent stablecoins, such as Tether (USDT) and USD Coin (USDC), are issued by centralized entities that retain full control over issuance, redemption, and the ability to freeze funds. This centralization directly contradicts the original ethos of decentralization within crypto, where permissionless and trustless systems were meant to disrupt traditional financial intermediaries.

Stablecoins, therefore, are not true representations of decentralized finance. Rather, they are digital IOUs backed by fiat reserves, issued and controlled by centralized companies. These entities comply with government regulations, respond to law enforcement requests, and manage reserves in accordance with external policies. This means users must place trust in these centralized issuers, effectively negating the decentralizing benefits that blockchain technology promised in the first place.

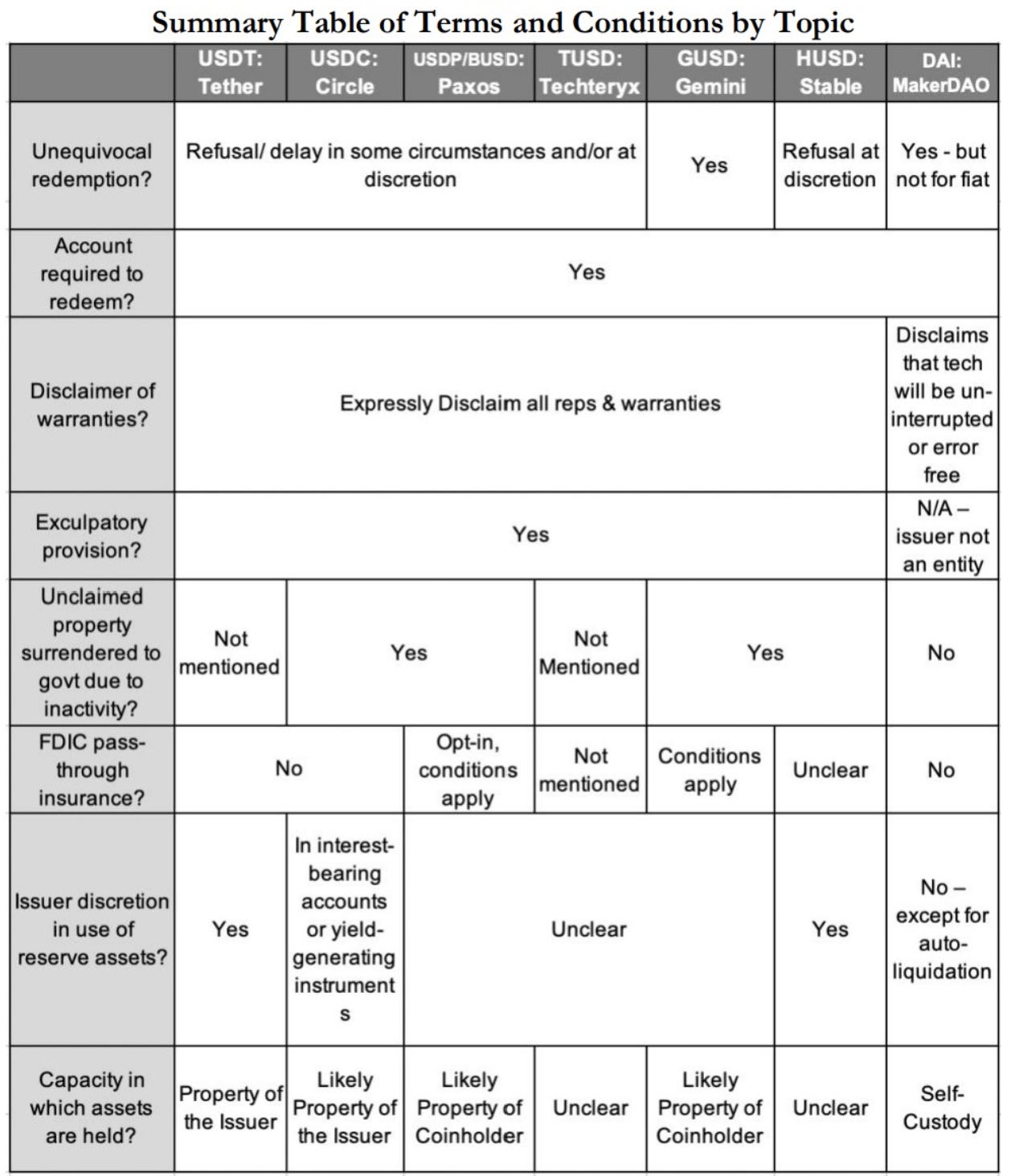

This centralization also means the user trusts the issuer to properly manage risk 24/7/365. And what do we mean by risk? Just take a look at the table below or this “risk scorecard” by BlueChip.org.

The proliferation of stablecoins across every major Layer 1 blockchain has introduced “capture risk,” in which the behavior and functionality of those blockchains become dependent on centralized entities subject to external influence.

Furthermore, the proliferation of stablecoins across various blockchains has led to fragmentation and redundancy. As more entities, fintechs, and even governments issue their own stablecoins, the market risks becoming a fragmented patchwork of incompatible systems. Instead of creating a unified digital dollar, we could end up with dozens of proprietary stablecoins, each adhering to different compliance standards and technical specifications. Without interoperability or unified standards, the very goal of stablecoins—creating a frictionless, global payment system—could be undermined.

Tether (USDT) exemplifies the centralization paradox in stablecoins. Despite facing scrutiny over the quality and transparency of its reserves, regulatory fines, and questions about its solvency, Tether has remained the dominant stablecoin globally. Its success can be attributed to several factors: it operates largely outside U.S. regulatory jurisdiction, issues primarily on Tron (a high-throughput, low-cost blockchain), and has integrated into peer-to-peer commerce in emerging markets like Brazil. Despite efforts by other stablecoins such as USDC and BUSD to displace Tether through greater transparency and regulatory compliance, Tether’s utility, speed, and access have made it the preferred choice for many users, particularly in emerging markets.

Tether’s paradox lies in its ubiquity despite the regulatory uncertainty surrounding it. While USDT dominates global stablecoin volume, it operates in a legal gray area, illustrating the tension between its utility in real-world applications and the lack of regulatory clarity in traditional markets.

Final Thought: Stablecoins Are Winning, but They Aren’t “Crypto”

Despite these challenges, stablecoins benefit from a powerful feedback loop. As more businesses, users, and financial institutions adopt stablecoins, the network effects grow, increasing liquidity and reducing the need for offboarding. Over time, stablecoins could function similarly to how Skype revolutionized global communications. Initially, users needed to rely on traditional phone systems, but as more people joined the Skype network, the need for landline systems diminished. In the same way, as stablecoin adoption increases, the need for traditional banking and payment infrastructure will decrease.

Stablecoins are entering a phase where more value circulates entirely within the stablecoin ecosystem, amplifying their advantages in cost and speed. This growing adoption could lead to a future where stablecoins become the dominant infrastructure for global payments, bypassing the inefficiencies and costs of traditional systems.

Stablecoins are poised to become one of the most adopted and impactful applications of blockchain. But in doing so, they may also compromise the original vision of crypto itself.

What Happens Next?

The stablecoin landscape has evolved from a speculative experiment to a vital bridge between traditional finance and blockchain-native infrastructure. As stablecoins continue to integrate into fintech, global commerce, and institutional frameworks, they are positioned to anchor a new era of programmable finance. However, their trajectory will be shaped by several key factors, including regulatory alignment, technological interoperability, and competition from central bank digital currencies (CBDCs). Below are high-conviction predictions that will define the stablecoin ecosystem in the next few years.

High-Conviction Predictions for 2025–2026

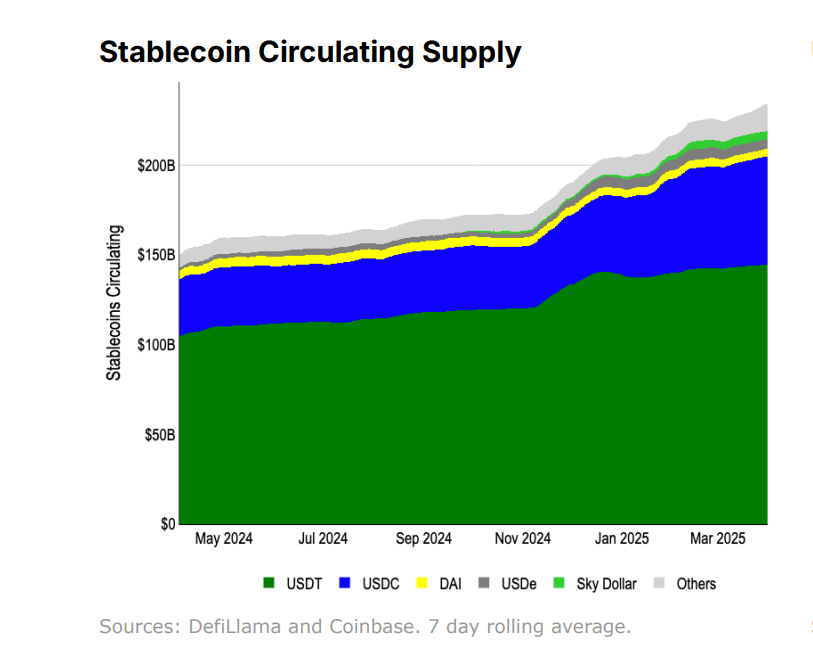

The Stablecoin Market Will Surpass $300 Billion in Circulating Supply

By Q1 2025, total supply exceeded $225 billion, driven by increased use in payments, decentralized finance (DeFi), and enterprise treasury management. With continued growth in adoption, analysts project the stablecoin market to surpass $300+ billion by 2026, positioning stablecoins as one of the most significant financial innovations of the next decade.At Least One G20 Bank Will Launch a Regulated, Branded Stablecoin

As fintech players like PayPal and Stripe enter the stablecoin arena, traditional financial institutions will follow suit. Banks such as Fidelity, HSBC, and Société Générale are already working on stablecoin initiatives. By the end of 2025, at least one major G20 bank will issue a fully regulated, fiat-backed stablecoin, leveraging its balance sheet and client base to compete directly with fintech-native issuers. This move will mark the beginning of stablecoins being integrated into the core of traditional banking operations.Stablecoin Networks Will Become Embedded in B2B Payment Infrastructure

Stripe’s acquisition of Bridge for $1.1 billion signals the growing role of stablecoins as the backbone of global finance. By 2025, stablecoin networks will be seamlessly integrated into mainstream treasury platforms, enterprise resource planning (ERP) systems, and cross-border APIs. This will primarily impact global e-commerce, digital services, and emerging market fintechs, which currently face high foreign exchange (FX) and settlement frictions. Stablecoins will become the default settlement layer for cross-border transactions, streamlining international payments and reducing operational inefficiencies.

CBDCs vs. Stablecoins: Convergence, Not Conflict?

While private stablecoins are moving ahead, central banks are cautiously advancing digital currency pilots. The digital euro, digital yuan, and the Bank of Japan’s CBDC trial will shape the future regulatory environment. The real question will be how CBDCs and stablecoins coexist in this new era of digital finance.

CBDC Advantages: Sovereign backing, central bank interoperability, and political support

Stablecoin Advantages: Programmability, composability, faster execution, and global liquidity

The most likely future is one of coexistence. Formal CBDCs for some nations while the U.S. may leverage USDC as a pseudo-CBDC. All the control without the scary name. Regardless, countries with restrictive foreign exchange (FX) policies or political concerns may resist the widespread adoption of stablecoins, while others may embrace them as a way to tap into global capital flows and digital economies.

Conclusion: Stablecoins Are the Rails, But Who Owns the Tracks?

Stablecoins are no longer just a bridge between fiat and crypto. They have become a rail system of their own, one that is faster, cheaper, and more flexible than the legacy alternatives. With programmable cash and composable infrastructure, they represent a first-principles redesign of financial value transfer, offering real improvements in capital efficiency, user experience, and market access.

But their rise also exposes hard truths. Most stablecoins today are neither decentralized nor permissionless. They inherit U.S. monetary policy, regulatory overhangs, and centralized control. As adoption grows, so too does the risk of regulatory capture, fragmentation, and mission drift. We may find ourselves with a system more efficient than the one it replaced, but no freer.

And yet, this is precisely why stablecoins are winning. They are useful. They work at scale. They solve real problems. For many, especially outside the global financial core, they are not a compromise; they are a lifeline.

The open question now is who will define their future. Will it be the crypto-native projects that birthed them? The fintechs and mega-platforms eager to adopt them? Or will it be the regulators and policymakers who seek to constrain them?

Stablecoins are no longer a speculative fringe idea. They are digital dollars, at internet speed, programmable, and portable. The infrastructure they are building may well define the next phase of global finance.

The only certainty is this: money is going on-chain. The rest is still up for grabs.

Usual disclaimer: I’m just some bloke in the desert. This isn’t financial advice, simply my thoughts in the most organized fashion I can muster.